CSRD insights from the EcoVadis webinar with EFRAG and Nexio Projects

CSRD insights from the EcoVadis webinar with EFRAG and Nexio Projects

June 26, 2025

Sustainability is not a static field. Ratings evolve, reporting standards shift, climate frameworks update, and regulatory requirements multiply. For sustainability professionals managing multiple frameworks at once, 2026 brings a particularly concentrated set of changes.

Nexio Projects’ multidisciplinary team spans ratings, reporting, climate, and regulation — and has translated the most important 2026 updates into resources you can use now. Here is the full picture: five frameworks, five updates, one guide.

EcoVadis is the world’s largest sustainability ratings platform, used to assess ESG performance across supply chains globally. Medal thresholds are becoming stricter each year, and 2026 is no exception. A score that earned a Gold medal last cycle may not do so this year, as the percentile requirements behind each medal tier are updated to reflect rising benchmark performance across the platform [1].

On the methodology side, three changes are central for 2026. Material topic customisation updates how the assessment is tailored to your sector, affecting which criteria carry the most weight in your score. New 360 Watch considerations change how third-party signals, including public records and external risk data, feed into your rating. VSME-aligned reporting introduces new possibilities for structuring your submission, particularly relevant for smaller organisations working within the EcoVadis framework.

Carrying over from 2025: higher requirements for the reporting indicator mean that evidence quality, not just policy existence, is increasingly determinative. Audits are now in place for specific certifications, adding a further verification layer for companies relying on third-party documents as evidence.

Download the guide → Stay ahead of the rising standards: EcoVadis 2026 unlocked

The UN Global Compact’s Communication on Progress is the annual reporting requirement for UNGC member companies, demonstrating commitment to the Ten Principles across human rights, labour, environment, and anti-corruption. The CoP questionnaire has been updated for 2026, and the changes go beyond form. They affect how companies perform against benchmark results and how their progress is read by external stakeholders [2].

The updated questionnaire places greater weight on how sustainability commitments translate into governance, strategy, and measurable action. Recent benchmark results have revealed consistent gaps across the member base, particularly on accountability structures and the depth of implementation behind policy commitments. The updated CoP also aligns more closely with GRI and the Sustainable Development Goals, making it increasingly useful as a cross-framework tool rather than a standalone reporting obligation.

For UNGC members, understanding the new requirements before your next submission and how to use the CoP as a strategic instrument rather than a compliance exercise, is the opportunity this update opens.

Watch on demand → From insight to impact: Changes to the CoP questionnaire

CDP runs the world’s leading environmental disclosure system, enabling companies to disclose data on climate, water, and forests to investors and supply chain partners. The 2026 disclosure cycle is coming up. See below the key dates in this year’s reporting.

2026 brings six headline updates to the questionnaire — and one structural change with particular significance [3].

For the first time, small and medium-sized enterprises can achieve an A score. That raises the competitive stakes of CDP participation across company sizes and makes leadership-level performance a more accessible target. Ocean disclosure is introduced as an optional, unscored module in 2026, signalling a direction of travel for future cycles. Changes also apply across the climate, water, forests, and plastics modules.

For companies managing multiple reporting obligations, CDP in 2026 is also an opportunity to reduce workload. The framework aligns closely with IFRS S2, CSRD ESRS, and TNFD, meaning data built for one requirement feeds directly into the others. Early preparation, before the disclosure window opens, is the most reliable way to improve score outcomes without increasing effort.

Download the factsheet → Ahead of CDP season: Guiding 2026 disclosures

Science-based targets have become a practical input into both regulatory compliance and supply chain credibility. The Science Based Targets initiative is updating its standard and validation process in 2026 — and for companies currently setting, validating, or reviewing targets, understanding what is changing is not optional [4].

The updates affect what “credible” target-setting looks like and what the validation process will require going forward. The session examines how the changes interact with the Omnibus regulatory landscape and what they mean for Scope 3 decarbonisation in practice — where the gap between stated climate ambition and operational execution most commonly appears. SB 253 readiness is also covered in context, for companies with California reporting exposure. For organisations building GHG inventories, the SBTi updates have direct implications for how that work should be structured to support both target validation and future audit readiness.

Watch on demand → SBTs in practice: The road to net zero and compliance

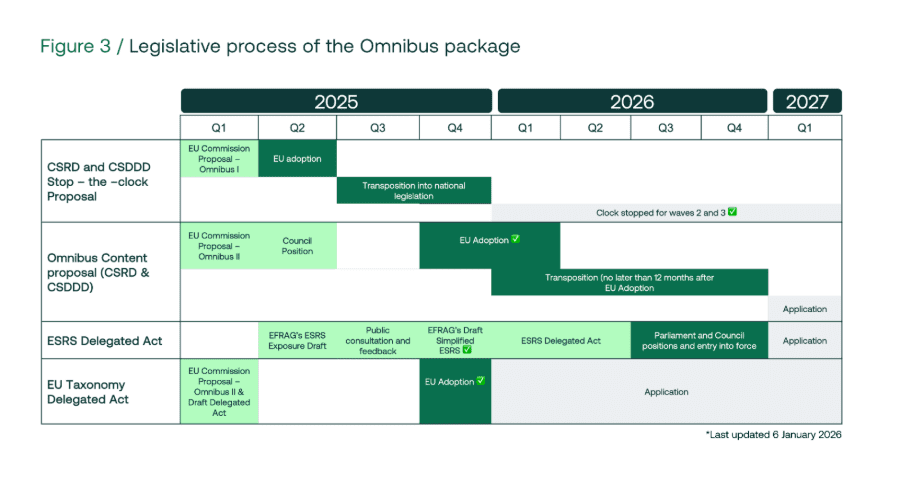

The Corporate Sustainability Reporting Directive has been amended. The EU published the final legally binding text of the Omnibus I Directive in the Official Journal, introducing scope changes, timeline shifts, and simplifications that affect thousands of companies across Europe [5].

The headline change: CSRD now applies to EU undertakings exceeding 450 million euros in net turnover and 1,000 employees, both thresholds must be met. Listed SMEs are now fully out of scope. Non-EU parent companies face their own revised thresholds and timelines. The simplified ESRS, removing more than 60% of current datapoints, is expected to be formally adopted by September 2026, with first reports covering the 2027 financial year due in 2028.

For companies still in scope, the revised timeline is not a reason to slow down. Double materiality assessments, ESRS gap analyses, and data systems take time to build properly and 2026 is the window to do it. For companies now outside scope, the commercial pressure from customers, investors, and supply chain partners has not eased with the regulatory threshold. Voluntary frameworks provide a structured path forward without the full compliance burden.

Read the article → EU Omnibus I finalised: What are the implications?

The sustainability landscape does not update once a year, it updates continuously. What makes the difference is not following every development as it happens, but having the expertise and partnerships to act on what matters, when it matters.

Nexio Projects’ team works across all five of these areas, with the depth and reach to support organisations wherever they are on their sustainability journey. Connect with the team to discuss which of these updates is most relevant to your organisation.

Numerous frameworks are moving at once. Nexio Projects’ experts are across all of them.

Get in touch to discuss what 2026 means for your organisation. Sign up to our newsletter to stay current as the landscape evolves.

[1] Nexio Projects (2026). Stay ahead of the rising standards: EcoVadis 2026 unlocked. https://nexioprojects.com/knowledge-centre/stay-ahead-of-the-rising-standards-ecovadis-2026-unlocked/

[2] Nexio Projects (2026). From insight to impact: Changes to the CoP questionnaire. https://nexioprojects.com/webinars/from-insight-to-impact-changes-to-the-ungc-questionnaire/

[3] Nexio Projects (2026). Ahead of CDP season: Guiding 2026 disclosures. https://nexioprojects.com/knowledge-centre/ahead-of-cdp-season-guiding-2026-disclosures/

[4] Nexio Projects (2026). SBTs in practice: The road to net zero and compliance. https://nexioprojects.com/webinars/the-road-to-net-zero-compliance-sbti-updates-and-sb-253-updates/

[5] Nexio Projects (2026). EU Omnibus I finalised: What are the implications? https://nexioprojects.com/eu-omnibus-i-finalised-what-are-the-implications/