CSRD updates: Timelines, legislative process, and what’s next

CSRD updates: Timelines, legislative process, and what’s next

September 26, 2025

Our recent webinar explored the EU Omnibus simplification package and its impact on CSRD reporting and wider ESG strategy. The focus was on understanding who is now in scope, how timelines have shifted, and what this means for both mandatory CSRD implementation and voluntary ESG reporting.

While the Omnibus has narrowed CSRD scope and adjusted the CSRD timeline, it has not removed the underlying regulatory and stakeholder pressure for high‑quality ESG and CSRD reporting. Instead, it has created a clearer differentiation between organisations in scope of CSRD and those that will move towards voluntary standards such as VSME or the soon-to-be developed voluntary standards for non-CSRD companies, and Global Reporting Initiative (GRI).

Download our reporting guide to understand the ESG reporting frameworks, relevant for your organisation!

The session summarised how the sustainability Omnibus package has evolved since the initial CSRD adoption in 2021. Four parallel legislative tracks were highlighted:

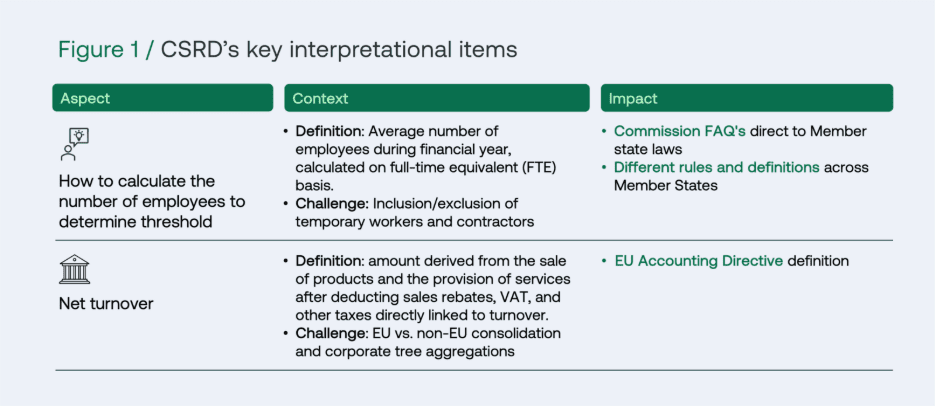

A key outcome of the Omnibus is the substantial increase in CSRD reporting thresholds.

CSRD:

CSDDD: Thresholds increased to 5,000 employees and EUR 1.5 billion turnover, clearly targeting very large groups.

Interpreting CSRD scope is less straightforward than the headline thresholds suggest. The employee criterion is defined as the average number of employees during the financial year, calculated on a full‑time equivalent (FTE) basis. This raises practical questions around temporary workers, contractors and part‑time staff.

Companies often struggle to calculate this consistently across Member States, particularly where national rules differ. Organisations are advised to reconcile definitions with the EU Accounting Directive and their financial statements. Similarly, net turnover must be carefully consolidated to determine whether thresholds are met at entity and group level.

Two new exemptions introduced by the Omnibus play an important role in CSRD scope and consolidation:

Both exemptions require transparent disclosure and do not remove the need to fully understand CSRD scope across the corporate structure.

Our experts have gone through practical case-by-case examples and scenarios to illustrate the complexities of determining CSRD applicability under three different scenarios:

To dive deeper into example scenarios, watch our on-demand session!

For organisations in scope of CSRD ESRS, a staged implementation journey aligned with the revised timeline is essential:

From financial year 2027, systems and tools must be ready for CSRD data collection, with reporting in 2028 subject to limited assurance and digital tagging.

For organisations not in scope, the focus shifts from compliance to strategic ESG positioning. Double materiality assessments remain highly valuable for ESG strategy, even without mandatory CSRD reporting.

Recommended actions include:

Small suppliers are not directly subject to CSRD, but larger customers may request sustainability data. Clients should not request information beyond voluntary standards such as VSME. Aligning reporting with VSME or GRI provides a practical response.

CSRD scope must be assessed at each consolidation level. Where consolidated thresholds are exceeded, a parent entity reports on behalf of the group, exempting subsidiaries from separate CSRD reports.

Significant events include any changes materially affecting IROs, such as mergers, acquisitions or divestments. These must be transparently disclosed where exemptions are applied.

Customers should not require data beyond voluntary standards. Suppliers aligned with VSME or GRI are better positioned to respond efficiently.

No. The Omnibus reinforces the strategic focus on business model and double materiality, encouraging a top‑down, strategy‑driven approach to ESG reporting.

Watch our session for more questions answered!

Nexio Projects supports organisations across their ESG and CSRD reporting journey, combining regulatory expertise with hands‑on implementation experience.

Key services include:

The objective goes beyond CSRD compliance, to using ESG and double materiality as drivers of strategic value creation and risk management.

If you’re interested in taking the next steps, book a free con sultation with our experts now. Discuss CSRD implementation, scope assessments, double materiality reporting or ESG strategy tailored to your organisation.

Additionally, you can subscribe to the monthly newsletter to stay informed on CSRD & ESRS developments, timeline updates and ESG reporting insights.