Earth Day: An update on the planetary boundaries

Earth Day: An update on the planetary boundaries

May 10, 2022

Many sustainability directors managing cross-border operations are now navigating a problem that could not have been anticipated three years ago: reporting obligations emerging simultaneously across different jurisdictions. A company with a UK parent, EU subsidiaries, and investors in ISSB-aligned jurisdictions such as Australia, Singapore, or Japan does not face one sustainability reporting mandate.

It faces three, each with its own language, timelines, and materiality logic. The challenge is that it’s easy to swing to either extreme: overcomplicating things by treating each regime as a completely separate workstream, or oversimplifying by assuming they’re interchangeable (for example, treating UK SRS and IFRS/ISSB as the same). Either approach can become expensive and potentially dangerous, without a preliminary impact analysis.

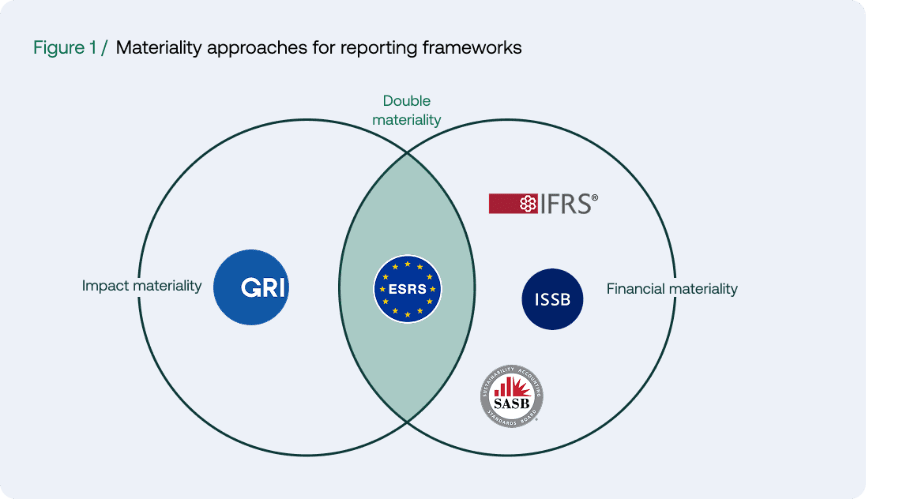

UK SRS (UK Sustainability Reporting Standards), CSRD with its European Sustainability Reporting Standards (ESRS), and the IFRS S1/S2 framework issued by the International Sustainability Standards Board (ISSB) share a common architectural spine. Organisations that recognise this can build one interoperable sustainability management system and scale it across jurisdictions. Those that do not will either spend three times the budget on three parallel processes that collect largely the same underlying data, or oversimplify the data collection and reporting requirements, leaving out key considerations.

The UK government published the finalised UK Sustainability Reporting Standards on 25 February 2026 (UK Government, 2026). The standards closely follow IFRS S1 (General Requirements for Sustainability-related Financial Disclosures) and IFRS S2 (Climate-related Disclosures), both issued by the ISSB in June 2023 , with targeted UK-specific adaptations to align with Companies Act requirements and UK listing rules.

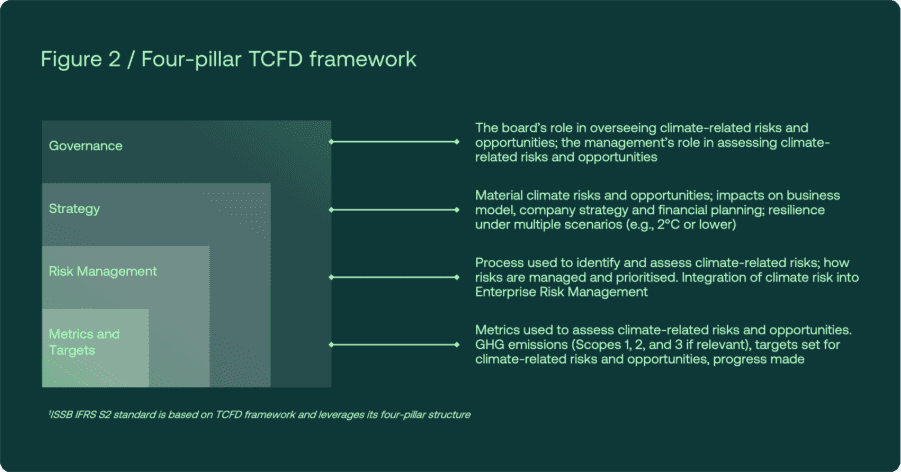

Similar to the IFRS architecture, UK SRS 1 covers general sustainability-related risks and opportunities: governance structures, strategy, risk management processes, and metrics. UK SRS 2 focuses on climate-related disclosures, following the structure of IFRS S2, which has taken over the mandate of the Taskforce on Climate-related Financial Disclosures (TCFD). The IFRS Foundation itself describes ISSB Standards as the culmination of TCFD’s work — the formal successor to a framework that is already mandatory for many large UK entities).

UK SRS is currently available for voluntary use. The mandatory route requires further regulatory steps. The Financial Conduct Authority published a consultation paper on 30 January 2026, with the consultation period closing 20 March 2026 and a Policy Statement expected Autumn 2026 for listed companies (FCA, 2026). Per the consultation paper, listed companies are set to report against the UK SRS as of 1 January 2027.

Private companies will be subject to a separate scope assessment. The direction of travel is clear: with the adoption of the UK SRS, the UK is building a mandatory ISSB-based regime and consulting on pace, not destination.

One practical detail matters early. UK SRS requires reports to align with financial statements from day one of adoption – no lag is permitted. Further, while companies are expected to report on UK SRS S1 and S2 at the same time, a climate-first transition relief allows organisations to report under UK SRS 2 before full UK SRS 1 application for the first reporting period, but the clock starts on adoption.

CSRD, underpinned by the 12 ESRS standards developed by EFRAG, applies to companies meeting size thresholds. Following formal adoption and publication in the EU Official Journal in February 2026, the Omnibus Directive raises the CSRD application thresholds to companies with more than 1,000 employees and €450 million net annual turnover, assessed at entity level and/or on a consolidated basis for EU parent undertakings. Member states have until 19 March 2027 to transpose these changes into national law.

For a detailed breakdown of what the Omnibus means for your reporting timeline, read our article.

Despite these differences, the IFRS Foundation and EFRAG are collaborating to increase interoperability between the two standards. The post-Omnibus ESRS revision has been undertaken keeping this in mind. The draft simplified ESRS introduces new concepts that increase interoperability with IFRS: such as fair presentation, materiality of information, and undue cost and effort.

However, proposed changes to the ESRS also include reliefs that go beyond the provisions of IFRS, thus reducing interoperability – e.g.reliefs for quantitative information on anticipated financial effects, deletion of certain previously mandatory data points etc.

All three frameworks are structured around the same four pillars inherited from TCFD: Governance, Strategy, Risk Management, and Metrics and Targets. This is not coincidental. TCFD influenced ISSB directly and EFRAG designed ESRS with ISSB interoperability built in (IFRS Foundation, 2023a; IFRS Foundation and EFRAG, 2024).

The practical implications are significant. A governance framework that defines how sustainability oversight is structured, and which disclosures flow from board and management-level decisions, satisfies the governance disclosure requirements of all three frameworks. A climate scenario analysis conducted to IFRS S2 standards satisfies UK SRS 2 and contributes substantively to ESRS E1 requirements. Scope 1, 2, and 3 greenhouse gas emissions data, collected once with appropriate methodology documentation, serves as the shared quantitative backbone across all three regimes.

A materiality assessment structured to meet ESRS double materiality requirements provides a strong foundation for the financial materiality dimension required by IFRS S1 and UK SRS 1, though the specific framing and outputs will need calibrating for each framework (IFRS Foundation and EFRAG, 2024).

The point is not that the frameworks are identical. They are not. The point is that the common elements are large enough that a single, well-designed sustainability management system can serve as the foundation, with jurisdiction-specific requirements layered on top without rebuilding from scratch.

The operating principle is straightforward: design to the most demanding standard, then calibrate for each jurisdiction.

The sustainability reporting landscape is converging. ISSB provides the global baseline. CSRD is the most rigorous expression of it for entities with European obligations. UK SRS is the UK’s endorsement of the same baseline, with mandatory adoption advancing (UK Government, 2026; IFRS Foundation, 2023a). The frameworks are not identical, but they speak the same language.

Organisations that manage these as separate compliance exercises will build parallel systems and bear the full cost of that duplication. Organisations that build from the common architecture – one governance structure, one data collection process, one materiality foundation – will find that CSRD, UK SRS, and IFRS S1/S2 obligations share enough common ground that one well-designed system serves as the foundation for all three, with targeted additions rather than parallel workstreams.

This is the transition from compliance to positive impact that Nexio Projects supports: Not managing sustainability reporting as a series of individual mandates, but as a single, coherent system connecting the needs of business and the planet.

Managing CSRD, UK SRS, and IFRS S1/S2 as separate workstreams is one of the most common and most avoidable mistakes we see. You have been handed multiple frameworks to deliver. The most important decision you make now is whether to build one system or three.

Nexio Projects works with sustainability directors and CFOs across the UK and EU to design reporting architectures that serve multiple frameworks from a single, assurance-ready foundation, without duplicating effort or budget.

European Parliament and Council (2026) Directive amending the Corporate Sustainability Reporting Directive (Omnibus I). Official Journal of the European Union. Brussels: European Union. Available at: https://www.consilium.europa.eu/en/press/press-releases/2026/02/24/council-signs-off-simplification-of-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness/ (Accessed: March 2026).

FCA (2026) Consultation Paper CP26/5: Aligning Listed Issuers’ Sustainability Disclosures with UK SRS. London: Financial Conduct Authority. Available at: https://www.fca.org.uk/publications/consultation-papers/cp26-5-sustainability-disclosures (Accessed: March 2026).

IFRS Foundation (2023a) IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information. London: IFRS Foundation. Available at: https://www.ifrs.org/issued-standards/ifrs-sustainability-disclosure-standards/ (Accessed: March 2026).

IFRS Foundation (2023b) IFRS S2 Climate-related Disclosures. London: IFRS Foundation. Available at: https://www.ifrs.org/issued-standards/ifrs-sustainability-disclosure-standards/ (Accessed: March 2026).

IFRS Foundation and EFRAG (2024) Interoperability Guidance between ESRS and IFRS Sustainability Disclosure Standards. London/Brussels: IFRS Foundation and EFRAG. Available at: https://www.ifrs.org/news-and-events/news/2024/05/ifrs-foundation-and-efrag-publish-interoperability-guidance/ (Accessed: March 2026).

UK Government (2026) UK Sustainability Reporting Standards: UK SRS S1 and UK SRS S2. London: Department for Business and Trade. Available at: https://www.gov.uk/government/publications/uk-sustainability-reporting-standards-uk-srs-s1-and-uk-srs-s2 (Accessed: March 2026).